Managing finances often feels like navigating a maze, especially for individuals striving for financial independence amidst economic uncertainties. An emergency fund is a crucial part of this financial landscape, serving as a safety net during unexpected events such as job loss, medical emergencies, or significant repairs. Picture this: You wake up one morning to find your car in need of costly repairs or you unexpectedly lose your job. In these instances, having an emergency fund can alleviate stress and provide stability. In India, the challenges faced in building an emergency fund can be profound. Economic fluctuations, market volatility, and unanticipated personal expenses can deter individuals and families from achieving financial security. With this context, we will explore the importance of an emergency fund, determine how much you should save, and what investment options will best serve this financial cushion.

Understanding Emergency Fund

An emergency fund is a sum of money set aside specifically for unforeseen circumstances that could lead to financial strain. This fund is a cornerstone of financial planning, providing peace of mind and steady footing during turbulent times. The necessity of having an emergency fund cannot be overstated: it allows you to handle unanticipated expenses without relying on credit cards or high-interest loans.

The size of your emergency fund depends on several critical components:

- Monthly Expenses: Calculate your fixed expenses—these include rent, utilities, groceries, and transportation. Knowing how much you spend monthly helps in determining the total fund size.

- Income Stability: If your job is secure with a reliable paycheck, you might lean toward the lower end of the recommended savings. However, freelancers or those working in volatile industries may require more extensive savings.

- Family Size and Dependents: If you’re supporting others, such as children or aging parents, consider saving more to cover their needs should an emergency arise.

Emergency funds play a vital role during economic uncertainty. They allow you to navigate job fluctuations, medical emergencies, and other unexpected life events without derailing your financial goals.

How Much Should You Save?

Industry recommendations for emergency fund size typically advocate saving between three to six months’ worth of living expenses. However, this can vary based on individual circumstances. Let’s break this down further:

- Basic Expense Calculations: Assess your monthly expenses, including rent, groceries, utilities, and transportation. Multiply this figure by the number of months you wish your fund to last. For instance, if your monthly expenses total ₹30,000, an emergency fund of ₹90,000 (for three months) to ₹180,000 (for six months) would be prudent.

- Personal Factors: Consider your personal situation:

- If you work in a stable sector like Public Sector or FMCG, where layoffs are less frequent, a fund covering three months may suffice.

- Conversely, if you are self-employed or in a start-up or in a sector like tourism which is susceptible to economic downturns, aiming closer to six months—if not more—may provide a necessary buffer.

Investment Options for Emergency Funds

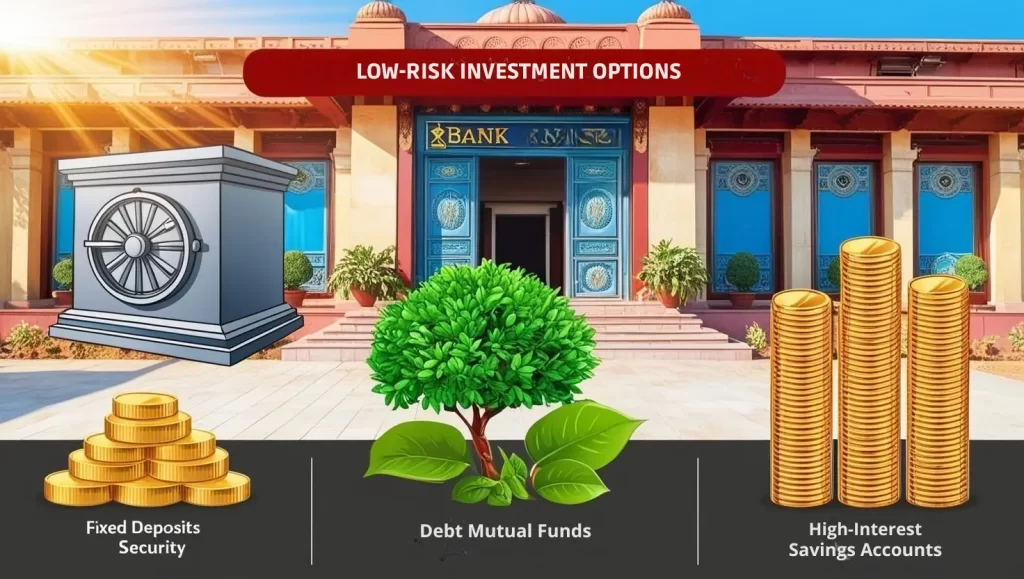

Now that you have a clearer understanding of how much to save, the next consideration involves where to keep those funds. The common goal is to achieve a balance between growth and liquidity—accessing your funds quickly while still earning some interest. Here are a few low-risk investment options to consider:

- Fixed Deposits (FDs): FDs are a popular option among Indian savers. They offer guaranteed returns and are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) up to ₹5 lakh per depositor. Typically, these accounts provide attractive interest rates, which can range from 5-7% per annum, depending on the tenure.

- Debt Mutual Funds: These funds invest primarily in fixed-income securities, providing a slightly better return than FDs while maintaining lower risk. They are relatively liquid, allowing you to access your funds in a short timeframe, making them suitable for emergency savings.

- High-Interest Savings Accounts: Some banks like IDFC First bank offer specialized accounts with higher interest rates designed for higher balances. These can serve as a liquid option for emergency funds while still earning some interest.

- Stable Stocks with Dividends: While it is advisable not to invest your emergency fund in equity, keeping a portion in stocks of companies like Coal India or BPCL that offer dividends can bolster your savings. Be cautious with this approach; ensure you understand the market implications and timing before leveraging stock investments for emergencies.

Conclusion

In conclusion, determining the appropriate size of your emergency fund involves a careful assessment of your financial situation, monthly expenses, personal circumstances, and market conditions. While standard guidelines suggest saving three to six months’ worth of living expenses, individual needs may vary.

The key takeaway is to prioritize creating a safety net that aligns with your lifestyle and financial obligations. Regularly review your emergency fund to ensure it remains reflective of any changes in your financial landscape.

Take control of your financial future by assessing your current financial situation and ensuring your emergency fund is adequately prepared. Subscribe to Stockastic and learn more about financial independence.

An emergency fund is a dedicated savings account designed to cover unexpected expenses or financial emergencies, such as medical bills, car repairs, or sudden job loss. It serves as a financial safety net, providing peace of mind and reducing the need to rely on credit or loans during unforeseen situations.

Having an emergency fund is crucial because it helps you manage unexpected expenses without disrupting your financial stability. It prevents you from accumulating debt and provides a cushion during financial hardships, ensuring that you can maintain your standard of living even when faced with unforeseen events.

Financial experts typically recommend saving between three to six months’ worth of living expenses. However, the exact amount depends on individual circumstances, such as job stability, income consistency, and personal responsibilities. For instance, if you have dependents or work in a volatile industry, you might consider saving more.